Opening An Account?

To become a member you must meet certain criteria e.g. live, work, study or attend school within our common bond. The following documents will be required to join:

- Photo ID - valid passport or driver's licence.

- Proof of Address - utility bill , bank statement or Government document dated within the last six months.

- Proof of working or studying in the area - Written confirmation on headed paper from Employer or College

To open an account for a minor under 16 the following documents will be required

to join:

- Birth certificate for the child.

- Childs Passport if available.

- Proof of Address - Parent(s) / Guardians(s) utility bill , bank statement or Government document dated within the last six months

Benefits of Membership

Flexible loan repayment options and competitive loan interest rates

96% loan approval rate

Online banking and mobile app to access your account anywhere, anytime

Fast, friendly, efficient service from our dedicated staff

Three easily accessible branches with parking

We don't charge transaction fees for saving or borrowing with us

All members are invited to our AGM, where they have a say in how we are run

Monthly newsletter, keeping you up to date with what is happening in your CU

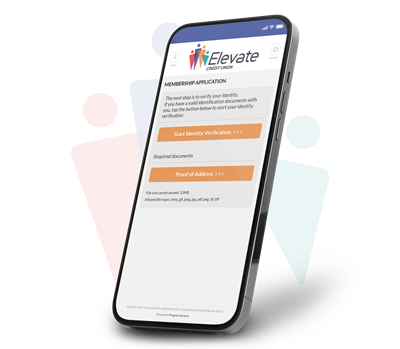

Join using your Phone

We’ve created an intelligent and secure method for you to become a member directly through your mobile phone. All you have to do is download our Mobile App to take full advantage of joining as you go.

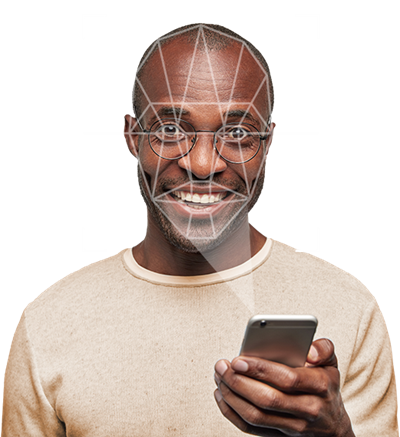

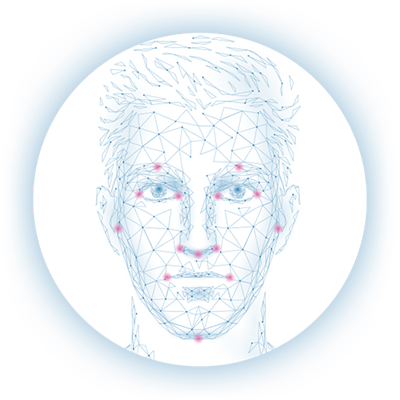

Secure Facial Verification

We use advanced biometric facial technology to capture and verify who you are. Simply take a quick selfie and you’re done. This intuitive technology, ensures becoming a member is quicker than ever.

Reliable Identity Check

We’ve created a way for you to share proof of ID with us that’s both secure and reliable. As you progress with your application, you will be given an opportunity to show your ID there and then. There’s no waiting around.

Quick Online Access

Once your membership has been approved, we'll text you a temporary pin so you can have immediate access to your online account. You won’t have to worry about anything, we will do the rest.

In order to start your Online Membership journey, you will need to download our Mobile App. To download our app today please either click/scan the QR Code or go directly to the App Store or Google Play Store.

How to get started

Download our Mobile App

Make sure you have valid ID ready

Complete the form

Verify your Identity

Upload required documentation

Sit back and wait for us to review and approve your membership

More Info

Have you received a letter from us looking for up to date Membership Forms, photo ID and/or proof of your current address? Under the Criminal Justice Acts 2010 & 2013, Elevate Credit Union Ltd. is required to obtain documentary evidence to confirm a member's identity at their residential address.

Acceptable Photo ID: Current valid Passport, current valid Driver's Licence, current valid EU National ID card. Acceptable Proof of Address: Bank Statement, Utility Bill or letter from a Government Department, showing your name and address and dated within the past 6 months.

If you have received a letter from us requesting these documents, your account needs to be updated. You have a number of options to do this.

- Come to any of our three branches with the original document(s) where one of our Member Service Officers will make a copy of these and update your account.

- You can email a copy of the requested document(s) to info@Elevatecu.ie. Please include a short note requesting your ID to be updated. If you email these documents, YOUR PHOTO ID MUST BE IN COLOUR.

- Post a photocopy of the requested document(s) to Elevate Credit Union, Doulgas West, Cork. Please include a note requesting your ID to be updated. If you are posting these documents, YOUR PHOTO ID MUST BE IN COLOUR.

**Please note that where we cannot obtain the necessary documentation from a member, we are required by law to place restrictions and cease providing services on accounts. In order to avoid this scenario, we would greatly appreciate your cooperation with this request.

A Dormant Account is an account which the member has not used in the past 3 years.

If you receive a letter from us saying your account is dormant, there is no need to join again. You're still a member! When an account becomes dormant, it doesn't close - your savings stay in the credit union and continue to earn a dividend at the end of each year.

What Are My Options If My Account Is Dormant?

- Reactivate your account. Come to any of our three branches with valid photo ID (passport or drivers license), proof of your address (dated in the past 6 months) and proof of PPS (this is on your payslips, p60 or social welfare card). You also have to lodge or withdraw some money.

- Close your account. To do this, you need valid photo ID and proof of your address. You can then withdraw the money in your account and close it.

- Transfer your account to another credit union. If you have moved from the area and you would like to move your account closer to your new residence, contact the credit union in your new area to make the transfer.

The European Union (Payment Services) Regulations 2018 (the “Regulations)

This is your ‘Framework Contract’ with us in relation to the particular payment account referenced

below and for the purposes of the Regulations to be given to you in relation to the particular account

referenced below. It is in addition to any other terms and conditions as may comprise or form part of

your Framework Contract with us and are applicable to such account (and/or any payments made or

applied on such account) as we may advise you of from time to time.

This document relates to the Credit Union’s provision of payment services excluding current accounts,

the terms of which are separate and available on the Credit Union’s website at www.elevatecu.ie.

Elevate Credit Union Limited is regulated by the Central Bank of Ireland.

Contact details for the Central Bank of Ireland are:

Address: New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3

Telephone: +353 1 224 6000

Fax: +353 1 671 5550

Website: www.centralbank.ie

CONTACT DETAILS FOR ELEVATE CREDIT UNION LIMITED

Address1: West Douglas,

Douglas,

Cork

T12 W950

Telephone: 021 4894555

Email: info@elevatecu.ie

Website: www.elevatecu.ie

Register Number: 46CU (the Central Bank’s register can be accessed on it’s website

www.centralbank.ie).

Sub Office Details : Supervalu Shopping Centre, Grange, Cork

Chapel Square, Passage West, Cork

Crestfield Centre, Riverstown, Glanmire, Co.Cork

27/29 Patricks Street, Fermoy, Co.Cork

Mainstreet, Watergrasshill, Co.Cork

Lower Glanmire Road, Victorian Quarter, Cork

2

Opening Hours :Monday to Friday 9.30am-5pm, Saturday 9.30-1pm.

Our business days are as follows: Monday, Tuesday, Wednesday, Thursday & Friday.

Saturday, or a public holiday in Ireland, are excluded from being a “Business Day” for the purposes of

the Framework Contract

YOUR ACCOUNT

The following is a description of the main characteristics of the account and payment services on the

account:

• Lodging and withdrawing funds

• Transferring funds internally to other accounts

• Acceptance of funds transferred into a members account by Standing Order/Electronic Funds

Transfer/Payroll Deduction

• Acceptance of funds transferred into a members account by Debit Card

• Once off Electronic transfer of funds out of a members account

• Online account access

• Bill Pay

• ATM withdrawal cards

1. Giving an order for payment from your account: When you give us an order to make a payment

from your account, we will need you to provide us with the details of the beneficiary of the

payment (i.e IBAN), together with any relevant identification details for the payment service

provider (‘PSP’) with which they hold their account). Depending on how you place your order with

us (i.e. online, in our offices, by telephone etc) we may also need you verify that order by

signature, by use of a password, or by use of a PIN, depending on the type of account that you

hold. All of this information, taken together, is known as the ‘unique identifier’ that you must give

us. In giving us that unique identifier, you will be consenting to our execution of that order for

you. You cannot withdraw that consent after you have given it to us. However, if the order is for

a direct debit to be taken from your account, you can revoke that order and your consent by

notice to the beneficiary of that direct debit up to close of business on the business day before

the funds are to be debited from your account. If the order is for a standing order to be taken

from your account, you can revoke that order and your consent by telephoning us or calling into

our offices up to close of business on the Business Day before the funds are to be debited from

your account. In exceptional cases, we may allow you to withdraw your consent after the times

specified above, but our specific agreement will be required and we will not be obliged to do this.

Elevate Credit Union now offers SEPA Instant Credit Transfers (SCT Inst). You can now receive SCT

Inst payments into your accounts. In order for you to receive an SCT Inst payment your payer (the

3

person making the payment to you) must send the payment through their Bank/payment service

provider as an SCT Inst payment.

Credit Union now offers SEPA Instant Credit Transfers (SCT Inst) allowing members to make euro

denominated payments within 10 seconds across SEPA-participating financial institutions. These

transactions can be executed 24/7/365, including weekends and holidays. To use SEPA Instant,

members must provide the recipient’s IBAN and confirm transaction authorisation through online

banking or in-office verification.

2. Cut-off times: When we are given an order in relation to a payment on your account, we must be

given that order before 10.30am on one of our business days. If we are given that order after that

time, we will be deemed to have received that order on our next following business day. If we

agree with you that an order is to be executed on a particular business day, then we will be

deemed to have received that order on that particular business day.

While standard SEPA credit transfers must be initiated before 10.30am on a business day for

same-day processing, SEPA Instant transactions will not have cut-off times and are processed

immediately.

3. Execution times: We confirm that we have up to the end of the first business day following the

date of deemed receipt under 2 above to so credit that amount. If the order is initiated by paper,

in both cases we will have an extra business day to do this.

• Standard SEPA Credit Transfer: Funds are credited to the beneficiary’s Payment Service

Provider (PSP) by the end of the next business day.

• SEPA Instant Credit Transfer: Transactions are completed within 10 seconds, ensuring

real-time payment availability.

4. Spending limits and payment instruments: If we give you a payment instrument on your account

(i.e. a card with a PIN number, or use of online banking with a password), you may separately

agree spending limits with us for use of a particular payment instrument.

If we give you such a payment instrument for your account, you must, as soon as you receive it,

take all reasonable steps to keep personalised security credentials safe. If the payment

instrument is lost, stolen, misappropriated or used in an unauthorised manner, you should notify

us by calling our main office on 021 4894555 during working hours. We reserve the right to block

your use of a payment instrument for any of the following reasons:

(a) the security of the payment instrument;

(b) if we suspect that it is, or has been, used in an unauthorised or fraudulent manner;

(c) (if the payment instrument is connected with the provision by us of credit to you) a

significantly increased risk that you may be unable to fulfil your obligations to pay; and

(d) our national or community obligations

4

If we block your use of a payment instrument, we will inform you about it (and the reasons for it)

by letter, email, secure online account messaging, text or telephone unless giving you that

information would compromise our security or would be prohibited by law. You may request that

we unblock the payment instrument, and we will do so, or replace the payment instrument, once

the reason for blocking no longer exists.

Subject to any other applicable limits, you can set personal transaction limits through online

banking or in-office service requests.

5. Charges: Currently accounts offered by Elevate Credit Union Ltd do not incur charges.

6. Interest rates: If an interest rate applies to your account, you are told this when you open your

account and that interest rate is incorporated by reference into this Framework Contract. You can

obtain confirmation of that interest rate by contacting us as set out on page 1 above.

7. Exchange rates: If any payment on your account (including a withdrawal by you from your

account) involves a currency conversion being made by us, we will use a reference exchange

rate that is determined by FEXCO international payments (the ‘reference exchange rate’). The

reference exchange rate will change daily and this is the basis on which we will calculate the

actual exchange rate. On the date on which we effect the currency conversion, we will take the

reference exchange rate that applies on that date, add a fixed amount of commission the total

will equal the actual exchange rate that is used by us in the currency conversion. You can find

out changes to the reference exchange rate by contacting us as set out on page 1 above.

SEPA Instant transactions are processed in EUR only. If a cross-currency transfer is required, it will be

processed using standard SEPA credit transfer rules, subject to applicable exchange rates and conversion

times.

8. Giving you information: If we need to communicate with you, give you information or notice of

any matters relating to this Framework Contract, we will do so by all means available to us at the

time including; in writing or by placing a notice in writing in our office and on our website. Such

information or notice will be given to you promptly upon the requirement to do so arising. You

may request that we provide or make available to you certain information (prescribed by law)

relating to individual payment transactions executed on your account at least once a month and

free of charge, in a manner that allows you to store and reproduce the information unchanged.

9. Copy Framework Contract: For as long as you hold this account with us, you have the right to

receive, at any time and on request by you, a copy of this Framework Contract on paper or, if

possible, by secure email.

10. Payment Errors and Unauthorised transactions:

If money is paid into or out of your Account in error, you agree to let us reverse the payment and

to correct the entries in your Account. If we do this, we do not have to contact you to tell you

beforehand.

In certain circumstances we may request your authority to recover a misdirected payment which

has been credited to your Account. If your authority is not forthcoming, we will provide such of

your details as may be required to the relevant Payer in order to assist their recovery of the

5

misdirected payment(s). If there are insufficient funds in your Account, then you will still be

responsible for the payment of this amount, to include any costs or expenses we incur.

Where any adjustment has been made to your Account through no fault of ours, you may have to

pay us any charges associated with doing this and we may take any amount you owe us from your

Account.

If you become aware of a transaction on your account that is unauthorised or incorrectly

executed, or if your payment instrument is lost, stolen or misappropriated, you must tell us

without undue delay and, in any event, within thirteen months of such a transaction being debited

from your account. You will be entitled to rectification from us if that transaction was

unauthorised or incorrectly executed. If the transaction was unauthorised, we will refund the

amount of it to you and, if necessary, restore your account to the state that it would have been

in if the unauthorised transaction had not taken place PROVIDED THAT:

(a) you will bear the loss of an unauthorised transaction on your account, up to a total of €50,

if the unauthorised transaction resulted from the use of a lost, stolen or misappropriated

payment instrument unless (i) the loss, theft or misappropriation was not detectable to

you prior to the payment and you have not acted fraudulently, or (ii) the loss was caused

by actions or lack of action by us or any of our employees, agents or third parties acting

on our behalf.

(b) you will bear all losses relating to an unauthorised transaction on your account if you

incurred those losses by acting fraudulently or by failing, intentionally or with gross

negligence, or if you failed to take all reasonable steps to keep the payment instrument

and personalised security credentials safe, to use the payment instrument in accordance

with any terms that we tell you are applicable to it, and to notify us without undue delay

of it being lost, stolen, misappropriated or used in an unauthorised manner;

(c) so long as you have not acted fraudulently you will not bear any financial consequences

resulting from the use of a lost, stolen or misappropriated payment instrument once you

have notified us in accordance with this Regulation 76 Information that it has been lost,

stolen or misappropriated.

11. Refunds of direct debits:

If a direct debit is taken from your account but:

(a) your direct debit authorisation did not specify the exact amount of the payment; and

(b) the amount of the payment exceeded the amount you could reasonably have expected

taking into account your previous spending patterns, this Regulation 76 Information and

other relevant circumstances; and

(c) you give us such factual information as we may require; and

(d) you did not give us consent in advance to the direct debit being taken from your account;

and

6

(e) neither we nor the beneficiary of the direct debit made information available to you about

the transaction at least four weeks before the debit date,

then you may request a refund from us of that direct debit. We will then have ten Business Days

to refund you, or give you reasons for our refusal to refund you and that your right to refer the

matter to the FSPO.

You may also request a refund for any direct debit payment for any reason for an eight-week

period following the debit date.

12. Unique identifier: If you give us an order to make a payment from your account and we execute

it in accordance with the correct unique identifier, we will be taken to have executed it correctly

as regards the beneficiary of that order. If you give us an incorrect unique identifier, we will not

be liable for the non-execution, or defective execution, of the order. We will, however, make

reasonable efforts to recover the funds involved.

To process a SEPA Instant Credit Transfer, members must provide the recipient’s International

Bank Account Number (IBAN). This is the unique identifier required to ensure the correct

execution of the payment. If an incorrect IBAN is provided, the transaction may be rejected or

misdirected, and recovery efforts will follow standard non-execution procedures

13. Our liability if you make a payment out of your account: If you give us an order to make a

payment from your account, we are liable to you for its correct execution unless we can prove to

you (and if necessary to the beneficiary’s PSP) that the beneficiary’s PSP received the payment. If

we are so liable to you for a defective or incorrectly executed order, we will refund the amount

of it to you and, if applicable, restore your account to the state that it would have been in if the

defective or incorrect transaction had not taken place. Irrespective of whether we are liable to

you or not in these circumstances, we will try to trace the transaction and notify you of the

outcome. If we refuse to execute a payment transaction, we will provide the reasons to you and

the procedure for correcting any factual mistakes that may have led to the refusal unless

prohibited by law or regulatory requirements.

14. Our liability if you receive a payment into your account: If the payer’s PSP can prove that we

received the payment for you, then we will be liable to you. If we are liable to you we will

immediately place the amount of the transaction at your disposal and credit the amount to your

account. If you have arranged for a direct debit to be paid into your account, we will be liable to

transmit that order to the payer’s PSP. We will ensure that the amount of the transaction is at

your disposal immediately after it is credited to our account. If we are not liable as set out above,

the payer’s PSP will be liable to the payer for the transaction. Regardless of whether we are liable

or not, we will immediately try to trace the transaction and notify you of the outcome.

If a SEPA Instant Credit Transfer is received into a member’s account, Credit Union will ensure

that funds are immediately credited and available for use, in accordance with EU Regulation

7

2021/1230. If there are any delays due to system outages or security checks, the Credit Union will

notify the affected member immediately.

15. Security and Fraud Prevention Measures: Due to the irreversible nature of SEPA Instant

transactions, Elevate Credit Union has implemented enhanced fraud detection and monitoring

measures. Members are encouraged to verify recipient details before initiating a SEPA Instant

transfer, as unauthorised transactions may not be recoverable.

When making a SEPA Credit Transfer or SEPA Instant Credit Transfer you may be asked to verify

the unique identifier and beneficiary details provided. This is known as Verification of Payee, and

it is important that you check the response provided by the PSP of the beneficiary. If you tell us

to proceed with a payment following the Verification of Payee response, we will rely on the details

provided by you and will have no liability to you if the details provided were incorrect.

If the Verification of Payee service is not available when it should be or if it incorrectly indicates a

match resulting in the incorrect execution of the transaction, we will refund you and restore your

account to the state it would have been in if the transaction not taken place.

For further details regarding SEPA Instant payments and compliance with PSD2 and SEPA Scheme

Rules, members can contact our support team or visit the Credit Union’s website.

16. Duration, changes and termination: Your contract with us, as detailed in this Framework

Contract, is of indefinite duration. If we want to change any part of the information provided

herein which is required by Regulation 76, we will give you at least two months’ written notice of

the proposed change where required by law to do so. If you do not notify us within that two

month period that you do not accept the proposed change, you will be deemed to have accepted

it. If you do not want to accept the proposed change, you must notify us in writing and you will

be allowed to terminate your contract with us in relation to the account to which this Framework

Contract relates immediately and without charge before the end of that two month period. If we

change an interest rate or an exchange rate in a way that is more favourable to you, we have the

right to apply that change immediately and write to you soon afterwards confirming that change.

We can change an exchange rate immediately and without notice if that change is based upon

the reference exchange rate agreed in this Framework Contract.

There are certain circumstances where we may give you shorter notice than two months or where we

will not tell you about changes or tell you about changes after we make them. This may happen where:

(a) the change is in your favour (e.g. where we reduce fees and charges on your Account or

change an interest or exchange rate in your favour);

(b) the change is required under law or regulation by a particular date, and there is not enough

time to give you the usual notice;

(c) the change is to introduce a new product or service that you can use in relation to your

Account;

(d) the change has no impact on the operation of your Account (for example, we make a change

to a term we use to describe something in this Agreement); or

8

(e) the change relates to certain benefits that may apply to your Account that are subject to

eligibility criteria and their own terms and conditions.

We can also change an exchange rate immediately and without notice if that change is based

upon the reference exchange rate agreed in this Framework Contract.

You may terminate your contract with us in relation to the account to which this Framework

Contract relates on one month’s notice in writing. We may terminate our contract with you in

relation to the account to which this Framework Contract relates on giving you two months’ notice

in writing.

17. Governing law and language: This Framework Contract shall be governed by and construed in

accordance with the laws of Ireland, and all communication between us and you during our

contractual relationship shall be conducted in English.

18. Redress: If you have a complaint in relation to the matters governed by this Framework Contract

you can write to us, and we will deal with your complaint in accordance with our obligations under

the Regulations. If you are not satisfied with the outcome of this internal process, you may refer

your complaint to the Financial Services and Pensions Ombudsman. Contact details are as follows:

Financial Services and Pensions Ombudsman Bureau, 3rd Floor, Lincoln House, Lincoln Place,

Dublin 2 D02 VH29. Tel. (01) 567 7000, E-mail: info@fspo.ie

19. Consent: By maintaining and/or carrying out transactions on this account, you explicitly consent

to us accessing, processing and retaining personal data necessary for the provision of these

payment services.